Africa's Fuel Markets Still Charge Over $3 Per Litre Despite Oil Price Decline

Quidah is an online platform that connects investors with curated opportunities and expert insights on Africa’s emerging markets, while offering businesses promotional services, partnership facilitation, and market intelligence to attract capital and grow their operations.

Industries

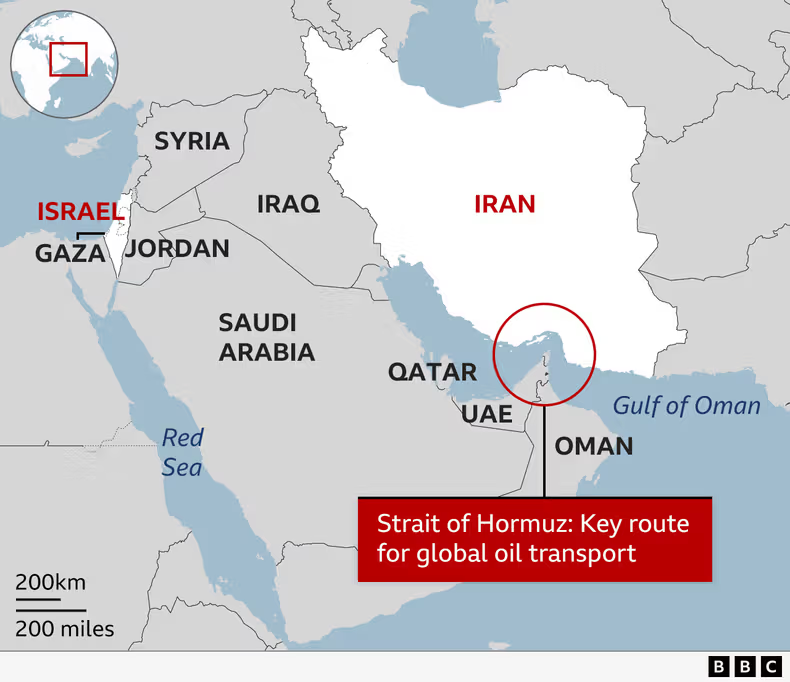

Despite lower oil prices following the easing of tensions in the Strait of Hormuz, fuel costs in some of Africa's most expensive markets remain stubbornly high, with motorists still paying more than $3.00 per litre. Global crude oil markets have eased after Brent fell back below $78 per barrel, reversing earlier spikes triggered by geopolitical tensions in the US–Iran conflict that at one point pushed prices close to $120 per barrel.

Retail fuel costs in Africa are mainly driven by import dependence, weak local currencies, and slow price adjustment mechanisms rather than just global crude prices. Countries like Nigeria, Malawi, Zimbabwe, Rwanda, and Senegal continue to experience some of the continent's highest fuel costs, with prices ranging from about $1.58 to $3.83 per litre depending on local conditions, currency strength and import dependence.

Domestic factors, such as limited refining capability and volatile exchange rates, prevent savings from cheaper crude oil from reaching African consumers. The disconnect between global crude oil prices and retail fuel costs is evident across multiple African markets, where domestic factors continue to outweigh international oil trends.

Nigeria offers one of the clearest examples. After briefly easing in late 2025, when increased competition and improved supply conditions pushed ex-depot petrol prices to around ₦699 per litre, prices reversed sharply in early 2026. By March, petrol had surged past ₦1,100 per litre and has since climbed to about ₦1,336 per litre (about $0.98), highlighting how domestic fuel costs can diverge from movements in global crude markets.

Elsewhere on the continent, the pressure is reflected in fuel price data. Malawi recorded the steepest increase among surveyed countries, with fuel prices rising from $2.02 per litre in January to $3.83 per litre in May. Zimbabwe also experienced a significant jump, climbing from $1.57 to $2.08 per litre over the same period. In Senegal, fuel prices edged higher from $1.64 to $1.65 per litre, while the Central African Republic remained relatively stable, moving from $1.87 to $1.88 per litre.

New entrants into Africa's most expensive fuel markets further illustrate the trend. Cabo Verde, Rwanda, Sierra Leone and Tanzania all ranked among the continent's top 10 costliest fuel markets in May, with pump prices ranging from $1.59 to $2.01 per litre. Analysts attribute these trends to a combination of currency weakness, import dependence, freight and refining costs, and domestic pricing structures.

Across the continent, three structural factors continue to drive the disconnect between falling global crude prices and stubbornly high retail fuel costs. First is import dependence. Many African economies still rely heavily on imported refined petroleum products due to limited domestic refining capacity. This exposes domestic markets not only to crude oil prices, but also to global refining margins, freight costs, and shipping insurance.

Second is currency weakness. Depreciating local currencies against the US dollar continue to amplify fuel import costs. As a result, even when Brent crude retreats from crisis highs, the local cost of fuel often remains elevated because petroleum is priced in dollars along the supply chain. Third is pricing structure and adjustment lag, where retail fuel prices tend to rise quickly during oil shocks but adjust downward more slowly when global prices fall.

The Petroleum Products Retail Outlets Owners Association of Nigeria (PETROAN) has urged refiners, depot owners and importers to immediately reduce fuel prices in line with the recent decline in global crude oil prices. Analysts say this pattern suggests that the key constraint is no longer just global oil direction, but the speed and structure of domestic price transmission. Until currency stability improves and import dependence is reduced, fuel markets are likely to remain only partially responsive to global oil relief.